Now let's talk about a few of the more undesirable aspects of MPI. Initially, MPI is a small part of the overall insurance market, and it is difficult to do online window shopping for the very best prices and terms. In addition, with MPI, all profits go straight to the lending institution, and MPI doesn't spend for anything beyond the mortgage quantity.

MPI likewise provides reducing advantages as the owner pays for the mortgage balance during life, although some companies offer policies that offer a level survivor benefit as an optional function. Because MPIs use ensured acceptance, the expenses of MPI surpass most term life policies, which require candidates to satisfy their underwriting requirements.

If you're home searching, or found your dream home currently, you may be wondering: Do I need to buy insurance coverage before closing on the house? House owners with a home mortgage need to buy house insurance. Mortgage lending institutions desire you to protect your home in case there are catastrophic losses. They provided you money so you might purchase your house and they still own a piece of it.

House owners without a home mortgage don't require home insurance. This is different from vehicle insurance coverage, which nearly every state requires. That said, it's still a sensible choice to have coverage, so your most likely biggest asset is safeguarded. As we pointed out, states do not require home insurance if you have actually paid off your house.

There is no minimum coverage like car insurance per se, said Elizabeth Enright Phillips, a previous certified residential or commercial property & casualty insurance representative and claims adjuster." There isn't a method to state, 'this is a dollar amount minimum' because of the large variations of danger aspects," Phillips stated about an absence of basic minimum requirements.

In most cases, your lending institution will have a "scope of coverage" that information what insurance coverage coverages you must bring. These requirements can differ by lending institution and location of the house however almost all loan providers will need that your house is guaranteed for 100% of its replacement cost. They wish to make sure the house can be completely rebuilt in case it is damaged.

After My Second Mortgages 6 Month Grace Period Then What Can Be Fun For Everyone

Various lending institutions have totally different requirements depending on the place, building codes, type of house, and so on. Home loan loan providers' primary concern is that your home insurance coverage protects against anything that can damage your (and their) possession. The lender appreciates the home, however doesn't consider the land, your valuables or other structures on the residential or commercial property.

They wish to make sure that your house is totally covered so that if it's harmed, it can be changed back to its present state and value." A home loan business is going to take a look at square video of the house and just how much it will require to reconstruct the home at that square video at that particular place in that market," Phillips stated.

As an example, if you paid $300,000 for your house with a $60,000 deposit, your lender may just need you bring $240,000 in insurance coverage. While this works fine for your loan provider (they will be made whole) if your house is damaged, you might not have enough insurance coverage to really restore your house.

Mortgage lending institutions likewise require liability insurance coverage. Liability insurance safeguards you if you're taken legal action against or somebody is injured in your house or on your residential or commercial property. Since your home is likely your most valuable property, a complainant may pursue your house. Your home loan business has a stake in that asset, which is why they require at least a minimum level of liability timeshare exit team reviews protection, which begins at $100,000.

If at some time throughout the years you end up securing a second mortgage on your http://collinlwzm671.trexgame.net/the-ultimate-guide-to-hawaii-reverse-mortgages-when-the-owner-dies home, you will likely face less stringent requirements for house owners insurance coverage. The second home mortgage loan provider has a smaller View website sized financial investment in your house and will assume you currently have actually the needed protection from your first home mortgage.

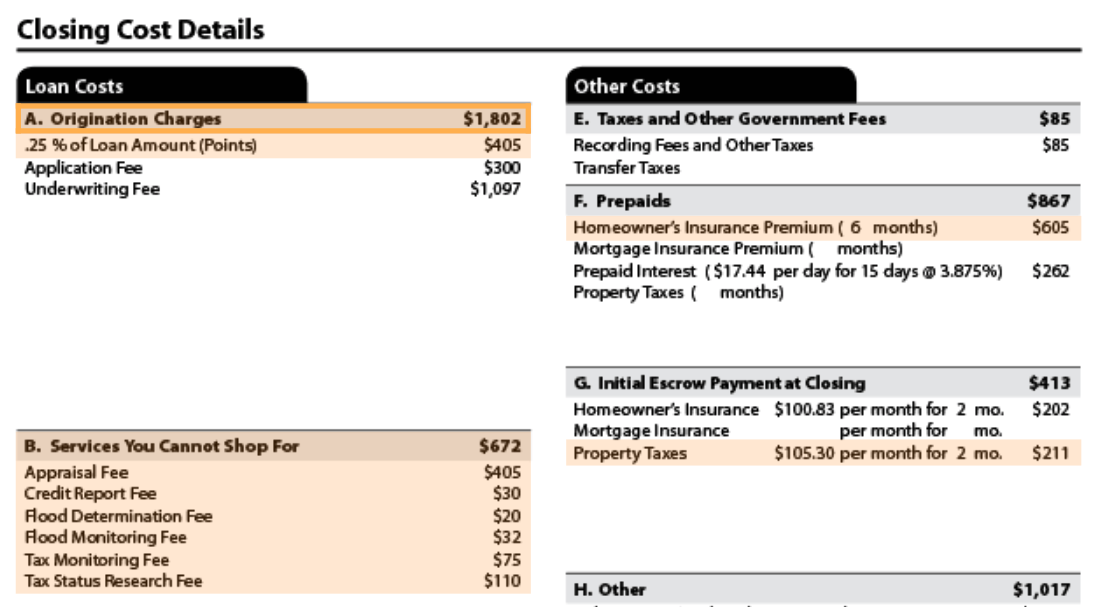

While it might appear like it's consisted of, it isn't. Your home loan and homeowners insurance coverage are 2 separate items. Frequently, your regular monthly home mortgage payment likewise covers your homeowners insurance premium due to the fact that your lending institution has actually set up an escrow account that manages your home mortgage payment, property taxes and property owners insurance. Despite the truth that you might only make one payment per month, that cash is broken up in between your home mortgage lender, state taxes and your property owners insurance business.

Top Guidelines Of Which Australian Banks Lend To Expats For Mortgages

All lenders require homeowners insurance in location before you close on a home. You will be needed to bring evidence of insurance coverage to the closing, by doing this the loan provider understands that their financial investment in your home is protected. Yes, if you have a mortgage on your house your lender will need that you have homeowners insurance in place.

They wish to make sure your house can be rebuilt or fixed in the event it is damaged or ruined. Your loan provider should alert you of their homeowners insurance coverage home mortgage requirements prior to closing so you can get a policy in location. If you own your home outright, you are not needed to bring house owners insurance.

Now, let's walk through the various types of protection in a house insurance coverage: This pays you to reconstruct or repair your home if it's harmed by a covered cause of loss, such as a fire. This covers what remains in your house, such as furniture, clothes and electronic devices. This assists pay your extra living expenses if you need to leave your house after it's harmed and while it's being repaired.

This might be due to the fact that of causing physical injury or property damage outside your home or if somebody is hurt on your property. This covers separated structures, such as garages, fences and sheds. A home mortgage lender may require additional protection if your home is thought about a risk. As an example, if your home lies in a flood zone or in an earthquake vulnerable area you might need to put flood or earthquake insurance in location.

Flood insurance plan can be acquired through the National Flood Insurance Program (NFIP) or private insurance providers. The cost of a policy differs considerably depending on your residential or commercial properties run the risk of elements. According to information from FEMA, the typical expense of flood insurance coverage has to do with $700 a year however that figure can increase considerably if you live oceanfront or on the coast.

If this holds true, you will need to acquire an additional windstorm policy that would fill this coverage space. Windstorm policies generally included a percentage deductible. If your home remains in an earthquake vulnerable location, your lender might need that you bring earthquake insurance coverage - how did clinton allow blacks to get mortgages easier. This is generally an included endorsement on your property owner policy or can be a standalone policy.

An Unbiased View of How Do You Reserach Mortgages Records

Your loan provider might need one or more extra endorsements to your insurance plan. A common request is water backup protection which helps protect your home from water damage due to overflowing sewers or drains pipes - how to rate shop for mortgages. In addition to specific coverage levels, your lender will likely require the following: The lender will need that they are named as a loss payee on the policy.